2 min read

The Rental Revolution: Overcoming Challenges in the Build-to-Rent Market

The real estate market has witnessed a significant transformation in recent years, with the emergence of build-to-rent. This innovative approach to...

4 min read

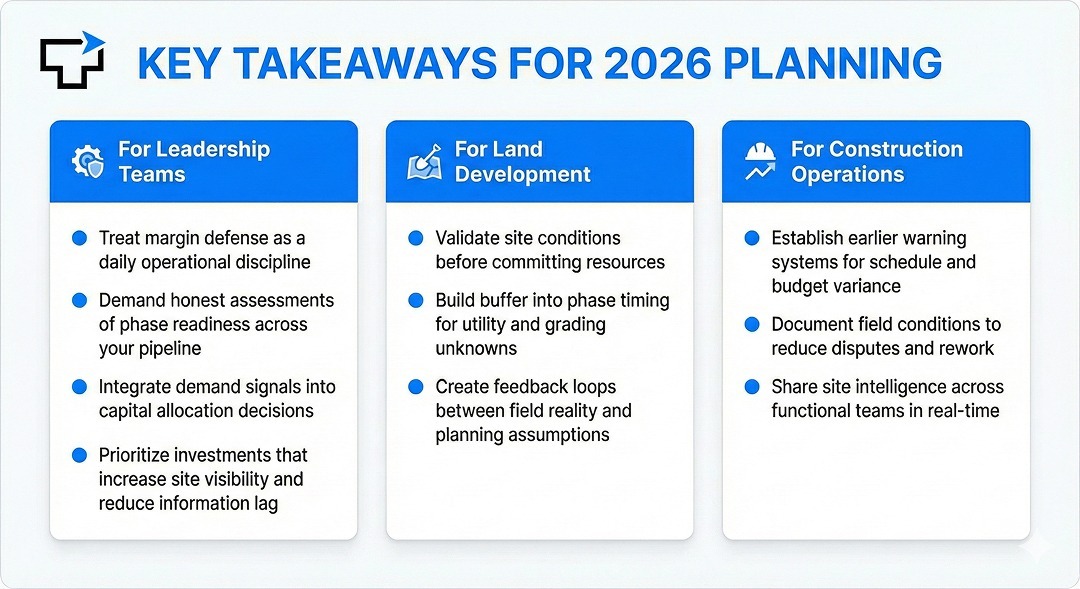

As this new year kicks off, leadership teams across the residential construction industry are facing a sobering reality: 2026 won't give builders much room for error. Margins are tightening, entitlements remain slow, investment capital is more selective, and the lots that actually move are harder to find.

But underneath the uncertainty, a clearer pattern is emerging. Builders who can identify issues sooner, align teams faster, and reduce avoidable risk are already separating themselves from the pack.

TraceAir CEO Ivan Lvov recently sat down with The Builder’s Daily Publisher John McManus for a forward-looking conversation about the year ahead. Five themes stood out as the forces that will shape 2026—and where builders still have leverage. Watch the full conversation here.

In 2026, margins aren’t just being nicked at the edges; they’re getting pressed from all sides all at once. Construction inputs remain expensive, even where materials have stabilized. The cost of money is higher, and lenders are more cautious than they were in the last growth cycle. At the same time, every delay, every rework order, and every missed inspection window shows up as a margin event, not just an inconvenience.

“2026 is going to be a year where homebuilders and their partners cannot afford invisible risk or invisible mistakes.”

The practical takeaway is simple but demanding: builders can’t assume the business will absorb slippage the way it used to. Every division needs a clearer line of sight from early assumptions to final gross margin. That means tighter control of scope, more realistic schedules, and better early reads on where risk actually lives. Teams that treat margin as something to defend daily—not just something to report quarterly—will be the ones who keep their numbers intact.

The industry likes to talk about being lot-starved, but that framing is incomplete. When you zoom out, most large builders control a meaningful pipeline of land. The problem is that only a slice of that pipeline is truly ready to move in today’s bumpy demand environment. On paper, the lots are there; in practice, entitlement friction, offsite dependencies, grading complexity, and utility bottlenecks create a much smaller pool of phases that can actually turn into starts and closings.

“The real constraint is the bottleneck of lots that are going to move and be desirable in this kind of bumpy, spotty marketplace.”

That gap between theoretical supply and real, buildable inventory is where profit is lost—or protected.

In 2026, land and development teams will have to get more honest about which phases are genuinely “ready,” which require additional work, and which should be slowed or rethought. That requires better visibility into dirt, drainage, utilities, and access before a phase is brought forward, not after crews are already mobilized.

Demand isn’t gone; it’s fragile and selective. Buyers are still in the market, but they are more sensitive to payment, location, and product fit than they were during the last run-up. Builders who treat demand as a blunt, top-down number will struggle. Builders who treat it as a set of signals will make sharper decisions about where and how to invest.

“Smart builders are using demand signals, online leads, and other traffic to decide which phases to bring on and which to hold back.”

Across the industry, leading teams are already using traffic patterns, online leads, spec turns, and cancellation behavior to decide which phases to start, which elevations to lean into, and which amenities are actually in high demand with buyers. That feedback loop is becoming a core part of land and product strategy.

In 2026, the divisions that win will be the ones that tie demand data directly into phase sequencing, plan mix, and site-level priorities—before budgets are locked.

The current environment is especially unforgiving for private builders and smaller groups with personal guarantees. When capital is tight and leverage is more heavily scrutinized, every misstep on land, development, and vertical delivery carries outsized consequences. A grading surprise, a utility delay, or a misaligned phase release isn’t just a headache; it can put real pressure on land covenants and builder cashflow.

“The cost of capital is higher, the terms are tougher, and the people borrowing — especially private builders — are carrying more risk.”

For these teams, the question is no longer “Can we tolerate surprises?” but “How do we eliminate as many surprises as possible?” That shifts the focus toward early clarity: understanding dirt balance before bids, validating utilities and drainage before starts, and catching issues that would have historically surfaced mid-stream.

In 2026, de-risking the front of the pipeline is one of the most powerful forms of protection a private builder has.

Underneath all of these pressures—margins, lots, demand, and capital—sits one lever that came up repeatedly in our discussion: visibility. The builders who perform best in a tighter market are the ones who can see more of the site, sooner, and share that view more effectively across their teams.

“When the pace slows a bit, that’s when companies finally have the time to improve their processes and take structural inefficiencies out.”

Visibility here isn’t a buzzword; it means being able to open a project and immediately understand how grading is tracking against design, where utilities actually sit in the field, how phases are progressing, and where schedule or cost risk is likely to show up next. It means replacing guesswork and “tribal knowledge” with something that’s inspectable: current surfaces, measurable quantities, documented changes, and a clear record of what happened when.

That’s where site intelligence platforms like TraceAir come in. By giving land and construction teams a shared, up-to-date view of the site, it’s possible to catch problems earlier, resolve questions faster, and make better decisions about what to do next. In a year when invisible risk is the most expensive kind, the ability to turn that risk into something visible—and manageable—is a real competitive advantage.

2026 won’t reward teams who simply push harder on the same processes. It will reward those who see further up the pipeline, reduce avoidable risk, and build systems that keep margins, schedules, and capital aligned. That means treating visibility as a core part of strategy, not an optional add-on.

For a deeper dive into the trends behind these themes—and how other leaders are responding—watch our full session on 2026 growth strategies for home builders.

2 min read

The real estate market has witnessed a significant transformation in recent years, with the emergence of build-to-rent. This innovative approach to...

Have a listen to their conversation as they discuss TraceAir's user-friendly technology, how science is similar to startups, and how we're making...

3 min read

Land acquisition teams across the country are in desperate search of lots to build on. The first quarter of the year has seen a significant...